Resources & guidance to help you

Make the most of your money

5 Things to Know About Paying for College

As close friends and neighbors have children heading into their senior year of high school, I can’t help but think about the fact that I will have a senior 2 years from now? It’s an exciting and emotional time for parents and students. During this swell of emotions, there are important practical considerations for senior year. “Someday my child will go to college” is now “my child is going to college next year”. College costs have skyrocketed. For 4 years of college, you can be looking at a total cost of $109,000 to $316,000. These numbers are daunting.

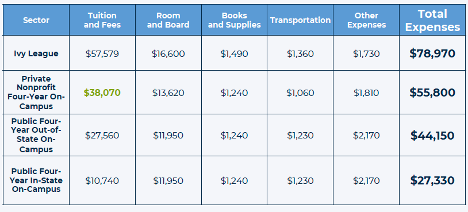

Here are some recent statistics on how much college costs on a PER YEAR basis:

If I had a senior this year, this is what I would want to know and understand from a financial perspective. For those of us with younger high schoolers, it’s helpful to be familiar with what is coming.

September 2022 to November 2022

This is the time that your senior is applying for admission and scholarships. If your child has a college that is her top choice, experts say it may benefit her to apply to other colleges that are known competitors for the same students, even if she has no intention of attending. This way you can pit them against each other in the spring for better financial aid. Who knew you could negotiate financial aid?? Not me! According to college aid experts, schools WILL NOT rescind your child’s admittance using this tactic. This is a common fear among students and parents.

During this season of football games and Homecoming, parents will want to discuss and prepare the following information:

1. Determine how much you are willing to pay for 4 years of college.

Try to put a dollar amount limit for all 4 years.

In my work, I find that most parents are NOT on the same page when it comes to how much they want the family to contribute to their children’s college costs.

Talk with your spouse, partner, or ex-spouse honestly about how much you want to contribute. Of course, all of us want our kids to come out of college debt-free, but that may not be a reality given the high cost of a college education these days. Nobody wants to limit their kids’ options based on money, but will you be sacrificing your quality of life or your financial well-being to make this happen? There is no right answer, but you and your partner need to understand the financial ramifications and be ok with whatever you decide.

If your family is struggling with this conversation, I recommend reading “The Price You Pay for College” by Ron Leiber. Questions like “What does your family value about college education?” and “What are the top 3 criteria that the school must have for you to feel good about where your child attends school?” can be a starting point. Click here to read a blog I wrote after a conversation with the author.

2. Determine how much you can actually afford to pay for 4 years of college.

No avoiding this step. No shame, no judgment. Get to a number.

- How much do you have saved for college right now? This includes any money or assets you have saved or earmarked for your child’s college costs, including your child’s 529 account and any UTMA/UGMA accounts.

- How much can you, the parents, plan to contribute each month to college costs?

- Will your child contribute to her college costs? If so, how much and how often?

- Will there be financial help from grandparents or other sources to help pay for college?

Add these numbers up to figure out how much you can realistically afford to pay for 4 years of college.

This information can be eye-opening and help you set reasonable expectations with your seniors of how much you plan to help them with college costs.

For those who have the financial means to pay for all 4 years of college without harming their retirement or lifestyle, that’s great! It doesn’t mean you have to pay for everything. Some parents find it beneficial if their student has “skin” in the game.

Here are some ideas I’ve heard parents have used:

- Pay for grades – College tuition and expenses are paid only if your student gets a 3.0 or higher (or whatever your expectation is).

- Promise your student that she gets whatever funds are remaining in her 529 accounts after she graduates from college. This can incentivize students to consider the value of their college choice, work harder for scholarship monies, and/or take more AP Exams in high school to gain college credit.

- Have your student pay for anything above tuition and housing – This can mean your student is responsible for expenses for joining the Greek system or her tab at the bar.

- Have your students take on federal loans at the beginning of college that delay interest payments until graduation. Then if they graduate with a certain GPA and/or in 4 years, you pay the loans off.

No right answers, just ideas. What other tactics have you heard other parents use?

3. Should you bother with applying for financial aid? If so, what should you know?

YES. Experts recommend that all seniors apply for financial aid through the FAFSA (“Free Application for Federal Student Aid”) on October 1, the first date they accept applications, or as soon as possible thereafter.

For parents who think they make or have too much money to qualify for financial aid, did you know that merit aid and scholarships often require the FAFSA form for your student to be considered? Merit scholarships and need-based grants pay for over 31% of college.[1] So what do you have to lose? The worst that can happen is your student does not get any money to help offset costs. You are exactly where you started. The best outcome is that your student gets to go to the college of her choice at a discount. Isn’t the hassle worth the possibility of saving thousands a year?

Applying early gives your student the best chance of getting money and getting the most money. Financial aid and merit scholarship dollars are limited and do run out.

If your senior is applying to private universities, check if the school prefers the CSS Profile for its financial and merit aid process. Here is a list of the schools and scholarship programs that use the CSS Profile. Like the FAFSA, you should create the CSS Profile on October 1, or as soon as possible thereafter. Keep in mind that there is a fee associated with submitting your CSS Profile to the school – $25 for the first school; $16 for each subsequent school.

If you are curious, here’s a link to an online calculator to see how much the FAFSA says you can afford to contribute to your child’s college education costs: Expected Family Contribution (EFC) Calculator.

December 2022 through February 2023

A lot of anxious waiting in these months…

March 2023 to Mid-May 2023

Your student starts receiving admissions and financial/merit aid package information. Yay!

4. Review the financial aid and merit scholarship offers to determine the net price (aka the real price you’ll pay) for each school that is smart enough to accept your child.

This is only one piece of information that will go into the hard decision of where your child goes to school. This is where discussions about what you and your family value about a college education are really important. What is worth paying for? Smaller class size? Alumni relations? Outstanding program for your student’s major?

This is the time you negotiate with schools’ financial aid departments.

5. Figure out how to fill the financial gap.

The gap is the difference between what you can afford to pay (Item 2) and the net price (Item 4). For most, this gap will be filled by some type of loan. I won’t go into the many types of loans out there. Generally, it’s preferable for the loan to be Federal, not only because of recent events, rather than private. It’s also preferable for the loan to be in the student’s name, not the parent’s name.

When thinking about how much your student should borrow, consider what a graduate in your student’s (current idea of her) major earns the first year on the job. The rule of thumb is the maximum amount of a student loan for all 4 years should be LESS than the starting annual salary for someone in her major post-graduation. You can check current annual salaries on the US Bureau of Labor Statistics. Experts recommend aiming for no more debt than the Federal Direct Stafford loan, which is $31,000.

Another way to think about loans is for every $10,000 in student loans that your student takes on, she will owe $100 per month for a standard 10-year loan. If she is unable to pay her loan in 10 years, she may be paying into well into her 40’s and 50’s with 3 times the interest.

This piece was intended to give you a general overview. There is so much information out there about how to pay for college costs. It’s overwhelming. You can find additional information at studentaid.gov or finaid.org. Hopefully, you now have starting point for family conversations about how much you plan to pay for college and how much will be the responsibility of your student. Please let me know if this has been helpful and if you have any questions that I can help answer.

[1] Sallie Mae, How America Pays for College 2019

Disclosures: BW Financial LLC dba BW Financial Planning is an Investment Adviser registered with the State of Colorado.All views, expressions, and opinions included in this communication are subject to change. This communication is not intended as an offer or solicitation to buy, hold or sell any financial instrument or investment advisory services. Any information provided has been obtained from sources considered reliable, but we do not guarantee the accuracy or the completeness of any description of securities, markets or developments mentioned. We may, from time to time, have a position in the securities mentioned and may execute transactions that may not be consistent with this communication’s conclusions. This communication is for informational purposes only and should not be construed as legal, accounting and/or tax advice. Should you have any questions and/or issues in these areas, please consult your legal, tax and/or accounting adviser.

CATEGORY

8/30/2022